Fashion is entering 2026 in the midst of its most significant reset since the pandemic, with the global industry, worth $1.7 trillion (£1.2tn), being reshaped by rising costs, changing consumer values and rapid advances in artificial intelligence.

All this is forcing brands to rethink not only what they sell, but how they operate, who they employ and how they earn customers’ loyalty.

The State of Fashion report, by Business of Fashion and McKinsey & Co, identifies nine major forces shaping the year ahead – but three stand out for UK consumers in particular: AI, wellbeing and resale.

AI Is Restructuring Fashion From The Inside Out

Artificial intelligence is no longer an emerging trend in fashion, it is already part of the supply chain. By 2030, up to 40 per cent of workers in developed economies will be expected to reskill as generative AI automates around a third of working hours across industries.

In fashion, this is already happening fast and out of sight in customer service, logistics and stock management, improving efficiency while exposing major skills gaps.

Crucially for shoppers, AI is also transforming how products are discovered.

Searches on generative AI shopping platforms grew by 4,700 per cent between 2024 and 2025, and 41 per cent of consumers now trust AI-generated search results more than traditional advertising.

In practical terms, this could mean fewer sponsored posts and more personalised, conversational shopping – and eventually AI “agents” that compare prices and even make purchases on our behalf.

Belonging Is The New Brand Power

British consumers have grown weary of dopamine-fuelled microtrends and endless product drops. The report shows a decisive shift towards emotional connection, depth and community, with almost nine in ten people saying that belonging to a like-minded brand community strengthens loyalty more than influencer marketing.

In response, brands are creating wellbeing-led “third spaces”: part retail, part social hub, designed to encourage people to spend time, not just money.

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

Go to website

ADVERTISEMENT

Get a free fractional share worth up to £100.

Capital at risk.

Terms and conditions apply.

Go to website

ADVERTISEMENT

While the trend is still emerging in the UK, it reflects a broader move away from buying more things and towards investing in lifestyle, experiences and connection.

With almost two-thirds (62 per cent) of consumers saying they feel an emotional connection to the brands they buy from most often, wellbeing is becoming a commercial necessity rather than a marketing add-on.

Globally, the wellness market is forecast to grow by up to six per cent annually through 2028 and British brands that embed it authentically will be best-placed to win loyalty in a squeezed market.

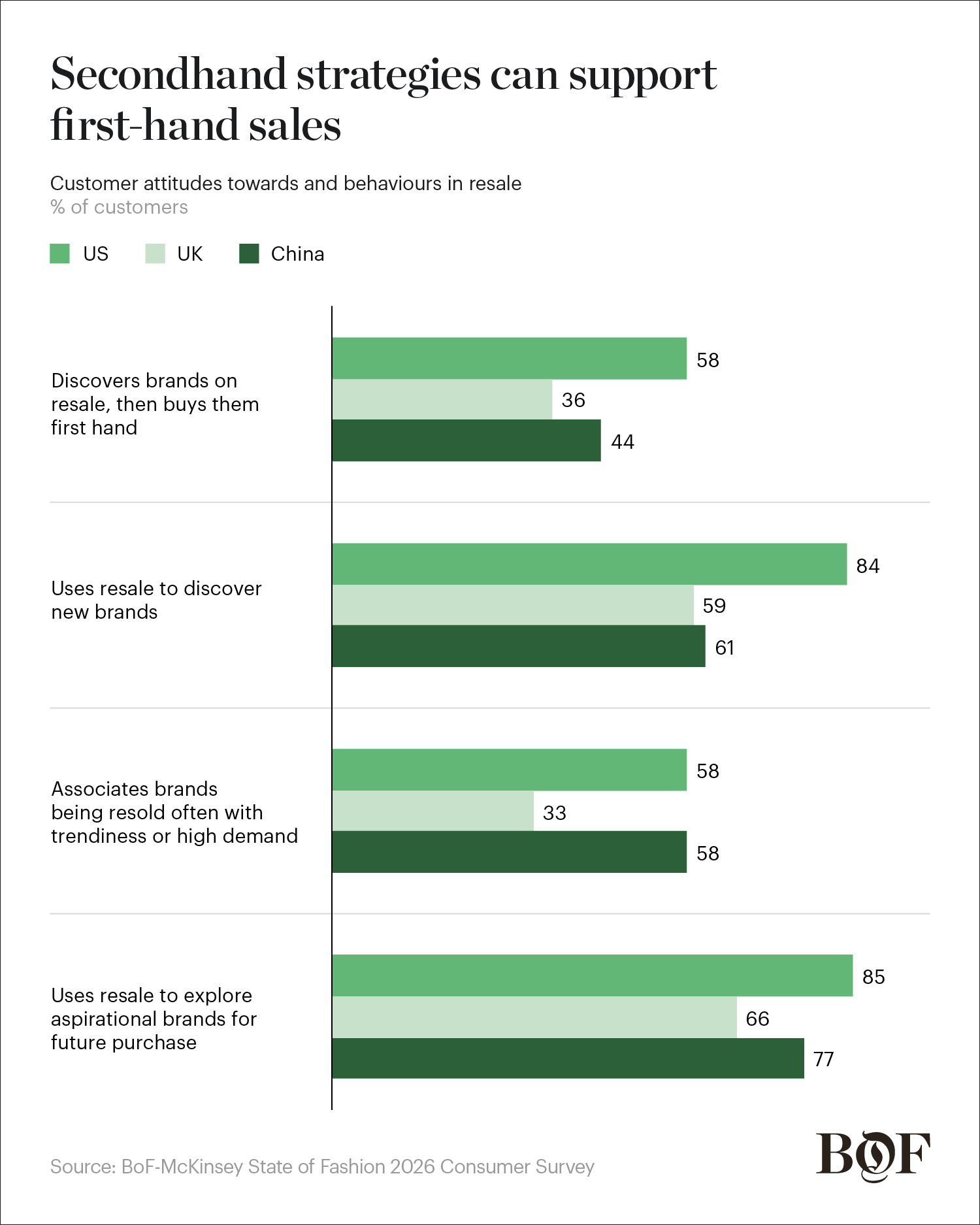

Resale Goes Mainstream

If there is one change UK shoppers can see and feel, it is the rise of resale. With household budgets under pressure, second-hand fashion is growing faster than the primary market, UK market leading the way with our long established love of charity shops, car boot sales and vintage finds.

In the UK, everyday and occasion wear dominate resale, from work staples to wedding guest outfits.

Platforms such as Vinted have become mainstream: the company returned to profitability in 2023, grew profits by more than 330 per cent in 2024, and by early 2025 became France’s biggest apparel retailer by sales volume. Nearly 60 per cent of global consumers say they are likely to shop resale in 2026.

Retailers are moving in too.

Selfridges’ Reselfridges combines trade-ins and specialist partnerships, as part of its ambition to make 45 per cent of its sales circular by 2030.

For shoppers, resale offers both value and a sense of ethical reassurance and for brands, it has become a strategic route to new customers and long-term loyalty.

All of this is unfolding against a challenging economic backdrop. Trade tariffs, rising duties and fragile consumer confidence are weighing heavily on the industry. Three-quarters (76 per cent) of fashion executives say trade disruption will materially impact growth in 2026, while 78 per cent identify falling consumer confidence as the biggest threat.

Yet there are glimmers of resilience. Nearly a third of consumers say they are still willing to “splurge” if the product feels right. Jewellery, for example, is outperforming other categories as shoppers gravitate towards pieces that feel meaningful, lasting and emotionally resonant.

At the same time, brands are becoming more efficient, moving upmarket to escape ultra-low-cost competition, and experimenting with new formats such as AI-powered smart eyewear, forecast to become a $30 billion global market by 2030.

The message from The State of Fashion 2026 is loud and clear. The brands that succeed in Britain will not be those chasing trends, but those offering genuine value: emotional, ethical and financial, in a world where how we shop is changing just as much as what we buy.