The Bank of England is expected to lower interest rates on Thursday after inflation fell to an eight-month low in November.

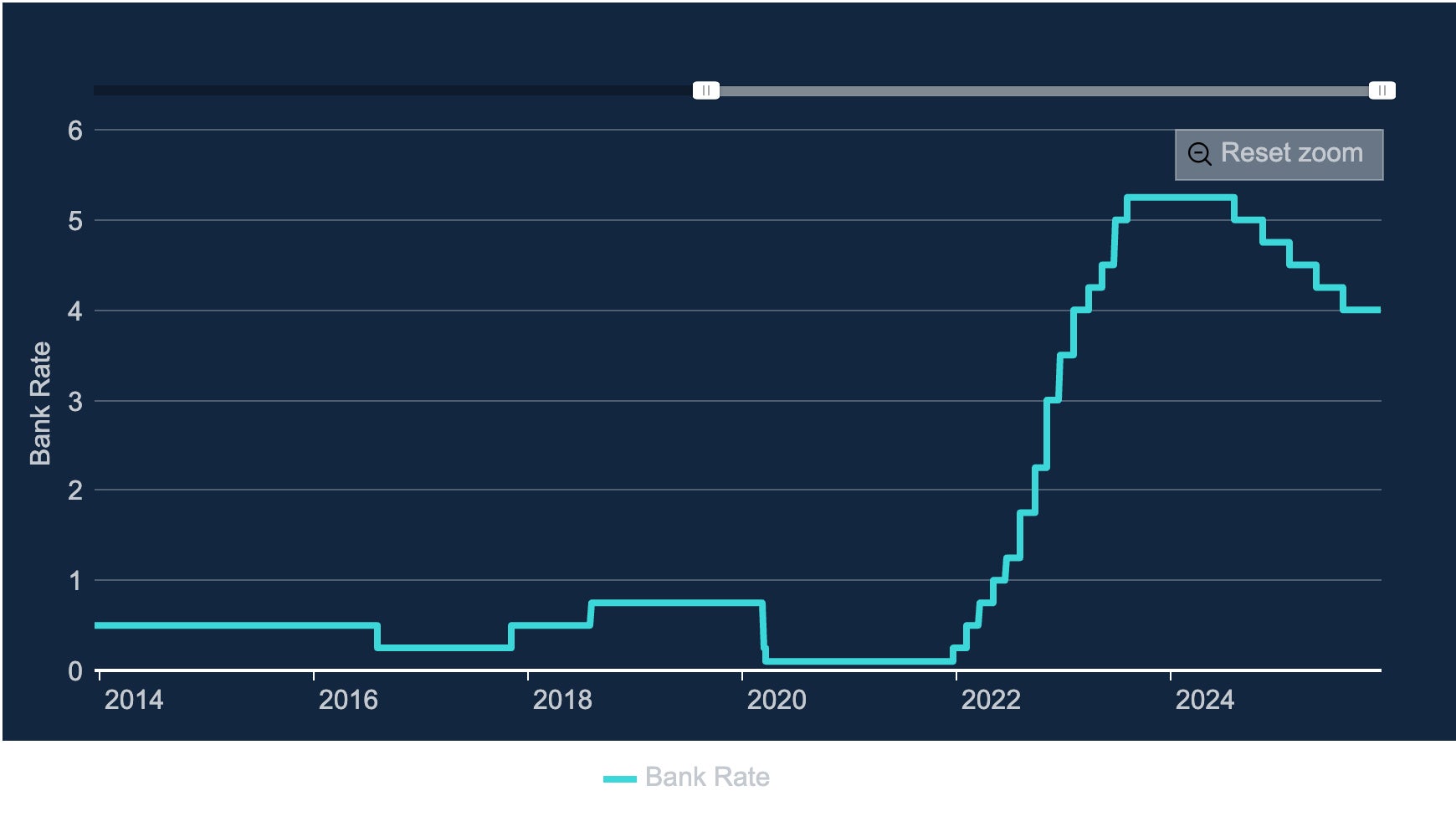

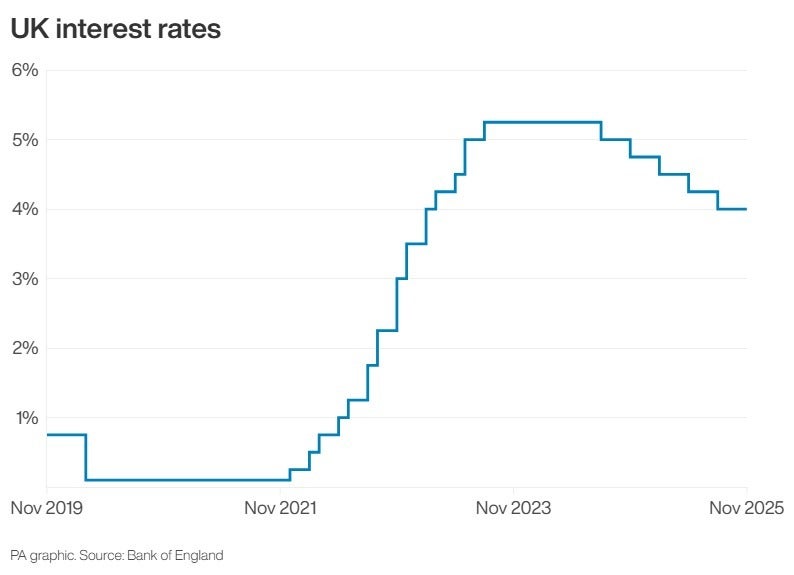

The Monetary Policy Committee is tipped to cut the base rate from four per cent to 3.75 per cent – the fourth such rate cut this year, following reductions in February, May and August. This would bring borrowing costs down to the lowest rate since the beginning of February 2023.

The rate of CPI fell to 3.2 per cent in November, from 3.6 per cent in October, the Office for National Statistics (ONS) said. This was largely driven by food and drink inflation, which dropped to 4.2 per cent from 4.9 per cent, while alcohol and tobacco prices also eased.

The BoE has been reluctant to make cuts due to lingering inflation, but the recent glut in economic data means a rate cut is all but certain, economists believe.

Last week, the UK economy was confirmed to have contracted 0.1 per cent in October, while this week showed unemployment rising, wage growth slowing and – most notable – inflation dropping to a lower level than expected at 3.2 per cent.

Results will be announced at midday on Thursday.

Will an interest rate cut affect my savings?

This question is a more immediate issue for many people. Savings rates have been pretty good for a couple of years now – that’s the flip side of rising inflation (which everybody hates), that interest rate increases mean you can earn money on your money (which everybody likes).

For quite a while we’ve been able to earn an easy 5 per cent or more in very basic easy-access savings accounts, but in the past few months that has dropped down to 4.5 per cent for only the very best accounts.

Most offer less already, and if you’ve not moved your money by now you’ve likely missed the boat for even those. Easy access accounts tend to be variable rate, which means they’ll move in tandem with the BoE’s rate.

If the MPC votes for a cut today, then many bank accounts will follow suit, lowering the rate you earn – which is why it’s important to keep moving your money to ensure you’re getting as good a rate as possible.

The major exception here is if you’ve locked money away in a fixed-term savings account (also called a fixed-term bond); in these, the interest rate at the moment you put your money in is the rate you’ll get for the full term, be it a year or two years or sometimes even more.

The negative is that you usually can’t withdraw your cash from these until the end of the deal; on the positive side though, you’ll still get that higher initial rate even if the BoE cuts interest rates multiple times during that period.

Karl Matchett18 December 2025 09:58

How do interest rates affect mortgages?

First thing to note is, your mortgage might not be immediately affected when interest rates change. If you are on a fixed rate deal, you’ll stay on whatever that rate is until it expires – typically two, three or five years, but it can be very different.

But for people on SVR (standard variable rate) or tracker mortgages, those deals should switch up straight away…so lower, in this instance, after a rate cut is confirmed.

The wider picture is the mortgage market: banks and building societies jostling for position and custom, trying to out-do each other with better rates, better terms and lower fees to attract you the next time you have to renew your mortgage deal.

With the UK property market being in a fairly poor state right now – lots of pre-Budget uncertainty made people hesitate when they might have been considering buying or selling up – that competition for custom has increased significantly, with a clutch of lenders such as Barclays, Nationwide, HSBC and Santander all offering plenty of deals at below 4 per cent interest.

Barclays last week offered one specific deal at 3.51 per cent, in fact. So how do they go lower than the BoE’s base rate?

That’s because mortgages are based on swap rates – essentially, expectations of future interest rate movements – and they are traded on markets with regularity, allowing lenders to move their own prices and products ahead of any change in the main interest rate.

Karl Matchett18 December 2025 09:44

What has impacted inflation figures?

The BoE doesn’t only consider inflation: economic growth, wages, employment rates and plenty of other factors in the geopolitical landscape can come into play.

But with a government-set target of 2 per cent inflation to aim for, interest rates tend to be left higher until inflation looks to be under more control and heading back towards its intended target.

Consumer Prices Index (CPI) inflation is usually the figure used as the headline number – that’s at 3.2 per cent now. But it’s important to also look at the CPI data which includes costs for running households (CPIH), and this was 3.5 per cent for last month. CPIH is the preferred metric for the Office for National Statistics (ONS), who are responsible for collecting and releasing the data.

Rising food and drink prices for much of this year and wage growth not slowing to comfortable levels have been problems hampering further rate cuts this year.

But food prices did drop in November, as did wage growth, while unemployment rates rose and the economy contracted 0.1 per cent – all this means interest rates should drop this time around.

Holly Evans18 December 2025 09:28

Risk that Bank of England ‘may need to play catch-up in 2026’

“UK price pressures are rapidly easing amid persistent softness in demand growth. We expect headline inflation to fall towards the BoE’s 2 per cent target over the course of next year,” said Peel Hunt chief economist Kallum Pickering.

Mr Pickering thinks the risk now is that the BoE has “fallen behind the curve and may need to play catch-up in 2026”.

“We will be paying careful attention to the voting pattern and forward guidance which accompany tomorrow’s BoE decision for a signal that the bank is ready to lean harder against downside risks,” he explained.

“Do not be surprised if the BoE sends dovish signals that it stands ready to lean against downside risks next year – implying cuts at successive meetings.

Holly Evans18 December 2025 09:08

Analysis: Interest rates cut will be notable after rampant inflation

Our business correspondent Karl Matchett writes…

Assuming the rate cut does indeed arrive, it’ll be a notable one: the lowest that the base rate has been for nearly three years, since it jumped from 3.5 per cent to 4 per cent in February 2023.

This year we’ve had three rate cuts already and the last time we had four or more in a single year was way back in 2008, when we had five in quick succession in the aftermath of the financial crisis.

Very different circumstances this time around thankfully, but rates have been high for a clear and difficult reason in the UK – rampant inflation, especially across 2022 and 2023.

Yesterday’s data showed CPI has dropped down to 3.2 per cent, but it’s still well above the target of 2%, which is why interest rates haven’t come down quite as quickly as some were hoping for.

Holly Evans18 December 2025 08:45

How rising inflation impacts your mortgage and savings

Inflation has been on a difficult path in 2025, initially dropping before surging back up from April onwards.

However, it appeared to peak over summer and the latest figures thankfully have inflation back on the downward path, with Consumer Prices Index (CPI) inflation rate falling back to 3.2 per cent in November.

While the rate is lowering, remember, that does not mean prices are coming down – it means they are rising more slowly than previously.

Read the full explainer from our business correspondent here:

Holly Evans18 December 2025 08:22

How did the FTSE 100 fare on Wednesday?

The FTSE 100 made strong headway on Wednesday, supported by a larger-than-expected cooling in inflation and a spike in the oil price.

The FTSE 100 index closed up 89.53 points, 0.9 per cent, at 9,774.32. It had earlier traded as high as 9,853.13.

The FTSE 250 ended 123.78 points higher, 0.6 per cent, at 22,164.76, and the AIM All-Share ended up 2.07 points, 0.3 per cent, at 751.48.

The soft UK inflation data sealed the Bank of England’s (BoE) expected interest rate cut on Thursday and increased the likelihood of further reductions in 2026, analysts said.

Holly Evans18 December 2025 07:55

Sharp drop in November inflation ‘green lights’ December rate cut

James Smith, developed market economist for ING, said the sharp drop in November inflation “green lights” a December rate cut.

“Christmas has come early for the doves at the Bank of England, with inflation coming in well below expectations in November,” he said.

Mr Smith said he was expecting inflation to edge higher in December, partly due to a seasonal spike in air fares.

However, he said the “latest drop in inflation fits into a broader body of evidence suggesting that price pressures are cooling”, adding: “We expect headline inflation to fall pretty close to 2 per cent by May.”

He is forecasting another two cuts to interest rates in February and April next year.

Alongside falling inflation, the MPC is expected to take note of other signs that the economy is cooling including rising unemployment, slower wage growth and stagnant economic growth.

Holly Evans18 December 2025 07:46

Still a ‘massive question mark’ over 2026 despite interest rates cut

Danni Hewson, head of financial analysis for AJ Bell, said: “Although 3.2 per cent is still way above the Bank of England’s target, it is expected to be the final piece in the puzzle which will enable rate setters to deliver their own festive gift to borrowers with an interest rate cut on Thursday.”

The Bank is tasked with bringing inflation down to the 2 per cent target level.

Ms Hewson added: “There are still massive question marks about what 2026 will bring and markets don’t expect the Bank of England to cut interest rates more than once or twice over the next year, so borrowers hoping to see a return to the ultra-low levels many people had become used to will have to adapt.”

Holly Evans18 December 2025 07:28

Bank of England poised for Christmas interest rate cut after inflation slows

Interest rates are set to be cut before Christmas after inflation fell to an eight-month low in November, economists think.

The Bank of England is widely expected to reduce borrowing costs to 3.75 per cent from 4 per cent when it next announces its next decision on Thursday.

This would bring borrowing costs down to the lowest rate since the beginning of February 2023.

Experts have said the Bank’s Monetary Policy Committee (MPC) will be encouraged by recent economic data to lower rates at its final meeting of the year.

In particular, the decision follows the release of the latest inflation data, which showed a bigger drop to Consumer Prices Index (CPI) inflation than analysts had been expecting.

The rate of CPI fell to 3.2 per cent in November, from 3.6 per cent in October, the Office for National Statistics (ONS) said.

This was largely driven by food and drink inflation which dropped to 4.2 per cent from 4.9 per cent, while alcohol and tobacco prices also eased.

Holly Evans18 December 2025 07:23